Get Rich Slowly

Get Rich Slowly

Do it for the people you'll leave behind.

Everybody begins talks about finance by saying “this is not financial advice”. I’m assuming that’s for legal reasons, so I’ll just repeat them. This is not financial advice.

Plenty of who I would describe as some of the more “mature” dissident right and libertarian-adjacent figures identify the simplest and most effective way to detach yourself from the regime: get money. Without money you’re more likely to need government subsidised healthcare, and as the green initiatives continue to wreak havoc on our energy whilst being scapegoated with “Putin’s price hike”, many Western governments are rolling out subsidy plans for heating bills. As they keep trying to forcefully obsolete food fit for human consumption, that will inevitably backfire and then they’ll conveniently need to nationalise all food production.

This is about the time when someone will say “Why are you talking about money? Clearly you just need 20 acres of land to build and equip your own house, get farm animals and heavy machinery, stockpile petrol, collect your own water, set up a solar energy capture and battery system, and you’ll be fine.” Well done, very smart. What do you need in order to buy any of that?

Something that Keynesians often have to be reminded of is that production precedes consumption. Internet tough guys need to be reminded that purchasing ability must precede purchases.

This “prepper” mindset is fine on it’s face, but I’ve been in enough fringe internet circles and for long enough to see how it leads so many men in their early-to-mid 30s to be completely blind to everything else, because they mistakenly think that a collapse would happen in a single moment just around the corner. You’ll know the person I’m talking of if you’ve ever tried to talk about the viability of cryptocurrency and can’t get through a sentence with being interrupted with the well-thought-out rant from a gentleman with tribal tattoos and wrap-around shades about how all you need is bullets, gold, and beans. Societal collapse is underway right now, and I think we’re still a long way off from you needing to fire homemade mortars at roaming gangs of 20+ people coming to pillage your Heinz vault.

This is what too many movies and not enough history leads you to envision the collapse of civilisation as. Once it has clearly begun, it often takes decades for a civilisation to crumble, in cases such as the Byzantine Empire it took centuries. For societies who bring collapse upon themselves (which is us) rather than being defeated in war, the ability to turn the tide and resuscitate the patient before it’s too late is much greater. You should indeed prepare for the worst, but don’t assume it’s a done deal until the curtains fall.

You ought to do something, that’s for sure, but you need to think long-term and not a one-stop Bass Pro Shop or Mountain Warehouse splurge. Your first step in providing for yourself and your family against increased tyranny and/or chaos is being smart with money. Is your money working for you, or is it sat idle in a savings account with its purchasing power being slowly eroded by inflation? You can buy gold, yes - and you should aswell - but that is essentially freezing your money. If you don’t have any money going to work and making you more money, that’s a problem, and the biggest reason why people who are poor stay that way.

The more money that you have, the more independent you can be, and that’s the name of the game. It’s too late to get in the lifeboats when the ship’s already underwater. Start now. A wise program for long-term growth is to invest half of your disposable income per month (after some non-essential spending) in stocks and bonds. A huge advantage in the modern day is that you don’t need to labour away for weeks on end picking the right ones, you can go straight to a reputable Mutual Fund.

If you’re not familiar with compound interest, let me explain: If you increased 5,000 by 10% the value is 5,500, an increase of 500. If you increase 5,500 by 10% you get a higher increase, this time of 550. Keep increasing it by 10% and the actual return is higher every time. Applied to investing, this means that the more you make, the more you continue to make.

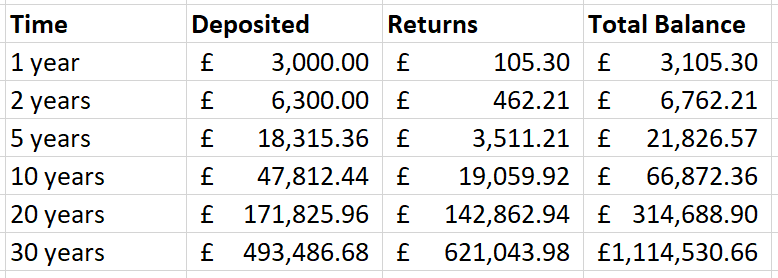

A stable Mutual Fund will have approx. a 5% annual return in stable years and (hopefully) a 10% return during years of high inflation. If we average out that to a 7.5% annual return, £250 deposit per month, with the deposit amount increasing by 10% every year to account for payrises, you get the following results:

This is absolutely not to be taken as a guarantee, it’s a blind estimate into the future and assuming a constant rate of return, which is fictional. But, from the moment you start depositing £250p/m, you could possibly become a millionaire 30 years later by doing nothing other than setting up a direct debit to a Mutual Fund. To some, that won’t seem particularly sexy. You’d be approaching retirement at that point or be past it. To others, the thought of having a net worth exceeding £1 million at any point in their life is jaw-dropping. But to me it ties in with something I’ve been thinking about a lot, that which is one of the most crucial reasons why we’re even alive: children.

When I think about why I want to work, succeed, settle down, be frugal, buy one nice home for life, pay off the mortage ASAP, it’s to become financially independent as soon as possible in order to accelerate this growth and provide more opportunities to my children than I could ever have dreamed of growing up. Getting them out of state schools, the NHS, and every other decrepit institution that I went through, and millions still will. I can’t save everybody from that fate, but I can save my children from it. And I can’t achieve the level of independence of a mountain man in my time here on earth, I can at least give my children the monetary means and some of the skills so they can have it if they need to.

If I do this and retire in 35 years my balance would be nearly exactly 2 million. After which I would no longer make deposits as I wouldn’t have an income aside from a pension. Not to worry, as even if I reduce my annual returns to 5% by holding safer assets, the yearly return would still be six figures. That would just keep going until I die, when it gets split amongst my kids who I’d teach to do the same with it.

The fruits of having a time preference this low extend beyond my own lifetime, and I am happy with that. Yes, this is providing I don’t have to yank it out due to a pending apocalypse and buy land within that time, but I’m willing to take that chance for the sake of the payoff.

And this can be poked and prodded all day about how it’s an unrealistic rate of return (it’s not but whatever), about how inflation takes purchasing power out of those returns, about the state of Mutual Fund providers, about how good gold is, on and on and on. But if you aren’t substituting this and getting your money to make money in another way, your critiques are empty.

If you aren’t already doing this, why not?

I have found (after only a week) that not being on twitter helps with this immensely. That cleverness used to write a funny tweet could have been used in an in person interaction, or in building a tool to automate parts of one's job.

This small difference adds up and puts your career exponentially further as time passes.